When’s a Good Time to Start a Family Office?

While new wealth may not seem complicated to manage, financial affairs can quickly become disorganized as individuals continue to accumulate wealth. This can lead to accounting and investing errors, which can be expensive and time consuming to fix.

There are four key indicators that suggest it might be a good time to set up a family office team.

- Invoice and transaction volumes become overwhelming, leading to late or inaccurate payments.

- You experience a liquidity event.

- The estate plan is confusing or hard to remember.

- Personal and financial privacy become an issue.

1. You or Your Bookkeeper Is Overwhelmed

In general, if you or your bookkeeper is overwhelmed, it’s time to hire larger financial management. This is especially true if you anticipate making more money through assets and investments, but don’t have the time or desire to manage your personal operations.

Monitoring the financial operations and output for each of your assets can be complex and time consuming, especially if you invest large amounts of cash in property, household employees, and businesses. What’s more, managing your finances incorrectly can lead to significant consequences, such as unintended gifts.

2. You Experienced a Liquidity Event

Individuals often put together a family office team after a liquidity event. Not only can liquidity events be emotionally challenging, they can also introduce logistical issues for many families.

For example, liquidity events often create voids of people and resources. Many individuals apply their business’s employees, resources, and services to their personal finance and management—a structure they lose access to with the sale.

A family office team can reestablish those resources in a more deliberate way that’s directly linked to your personal goals.

3. Your Estate Plan Is Confusing

Estate planning is important to transfer assets to designated beneficiaries in the most tax efficient way. However, the legalese and various structures even with simple plans can get confusing and hard to remember.

Your legal and tax teams can create an effective plan, but if you don’t respect the plan or entity structure you can create unintended consequences, such as an ineffective transfer of assets or unintended gifts.

Your family office team is charged with understanding your full picture and your estate plan. This team can help guide your family to keep your plan on track limiting errors and unintended consequences.

4. Your Privacy Is Compromised

We often forget how much private information is floating around on the internet. Home addresses, recent significant property purchases, and other personal identifiable information can often be found with a simple search.

Individuals and families need to consider ways to keep information as private as possible. Your family office team can help insulate you and your family. Some ways to maintain more privacy are:

- Don’t use your home address. Your home address on checks, letters, and other material leads people back to your home. Instead consider a PO that forwards to your family office team.

- Consider an entity structure for purchasing large assets if possible. For example, an LLC that’s owned by a privacy trust.

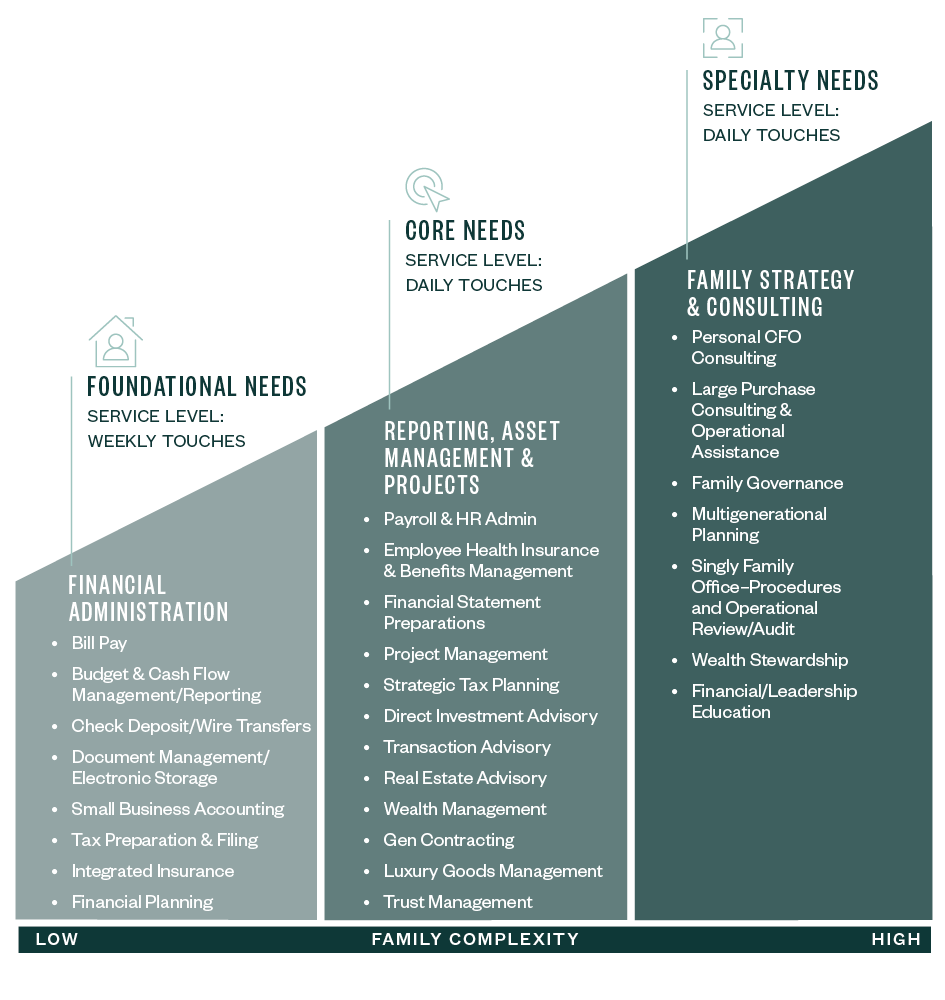

What Financial Needs Can a Family Office Meet?

An effective family office team can manage every aspect of your financial planning and operations, including:

- Personal and family financial needs, including estate planning and trust management

- Savings, investments, and philanthropy

- Cash management and cash flow, including bill pay, accounting, reporting, and household employee payroll

- Tax planning and coordination

Special-project considerations, such as buying a house or getting a visa in another country

How Do You Start a Family Office?

The following steps can help you set up your family office with confidence.

- Identify your needs and pain points. These might include cash flow and operations, legal, investment, and tax.

- Determine how much you want to invest in the family office. Family office teams can be expensive. Do your needs warrant a single-family office where you employ all team members, or an outsourced solution or a hybrid of both?

- Find your team.

Your Team: Who Should You Include in Your Family Office?

When setting up a family office, it’s important to pick an experienced team of advisors. Your team should be able to make recommendations, help you figure out what to do with your finances, and give you piece of mind.

Here are a few key members a strong family office team should include:

- Family office operations team. This is the team that controls the spend, payroll, expense reporting, and document management. This team keeps you organized and moving forward with your goals. This team often works as the backbone or coordinator of the overall family office.

- Investment team. Your investment team manages investments and overall investment reporting. This group can be internal or an outsourced firm that plays a role in your overall asset allocation as well as a client’s focus on direct self-managed investments.

- Legal team. The legal team is generally outsourced in a hybrid model. It should be a team of people you trust that can assist with various common topics, such as household employee issues, real estate, estate planning, and entity formation.

- C suite. The C suite is the overall advisory executives that pull the various teams together and report to the principals. This team can consist of several individuals in different capacities as in a business, but it often consists of one or two main individuals who you respect and trust to lead the entire family office enterprise.

We’re Here to Help

To learn how you could potentially benefit from a family office, contact your Moss Adams advisor.

You can also learn about additional opportunities available to individuals and families, such as estate planning, steps to strengthen your family’s financial position over generations, and more.